Main Points :

- JPMorgan is weighing loans secured directly by clients’ Bitcoin and Ether, expanding beyond its existing crypto‑ETF–collateral program.

- The bank now publicly backs stablecoins and tokenized deposits; it forecasts the stablecoin market at roughly $500B by 2028, far below some trillion‑dollar bull cases.

- Other U.S. megabanks—Citi and Bank of America—are rolling out or exploring stablecoin/tokenized‑deposit rails, signaling a coordinated TradFi shift.

- If implemented, crypto‑collateralized credit lines let funds and corporates unlock USD liquidity without selling core positions—an on‑ramp for new DeFi/TradFi hybrid products.

- Builders should eye: (1) collateral management/oracle tooling, (2) tokenized credit facilities, (3) KYC’d liquidity pools, and (4) real‑world‑revenue strategies around stablecoin flows.

1. A Turning Point in Wall Street’s Crypto Posture

JPMorgan Chase, long led by CEO Jamie Dimon’s vocal crypto skepticism, is reportedly preparing to let select clients post Bitcoin (BTC) and Ether (ETH) as collateral for fiat loans as early as 2026. The Financial Times first flagged the internal discussions; Reuters, Yahoo Finance, and CoinDesk quickly corroborated. This goes beyond the bank’s June move to accept crypto ETF shares as collateral—now we’re talking about the underlying assets themselves.

For institutional holders, the appeal is obvious: maintain long‑term crypto exposure while tapping dollar liquidity. For JPMorgan, it’s a fee stream secured by highly liquid, 24/7‑priced assets—if risk can be modeled properly. The shift also signals that “crypto risk” is being reframed as “market risk” like any other volatile collateral, provided custody, price discovery, and liquidation rails are robust.

2. Dimon’s Rhetoric vs. JPMorgan’s Balance Sheet

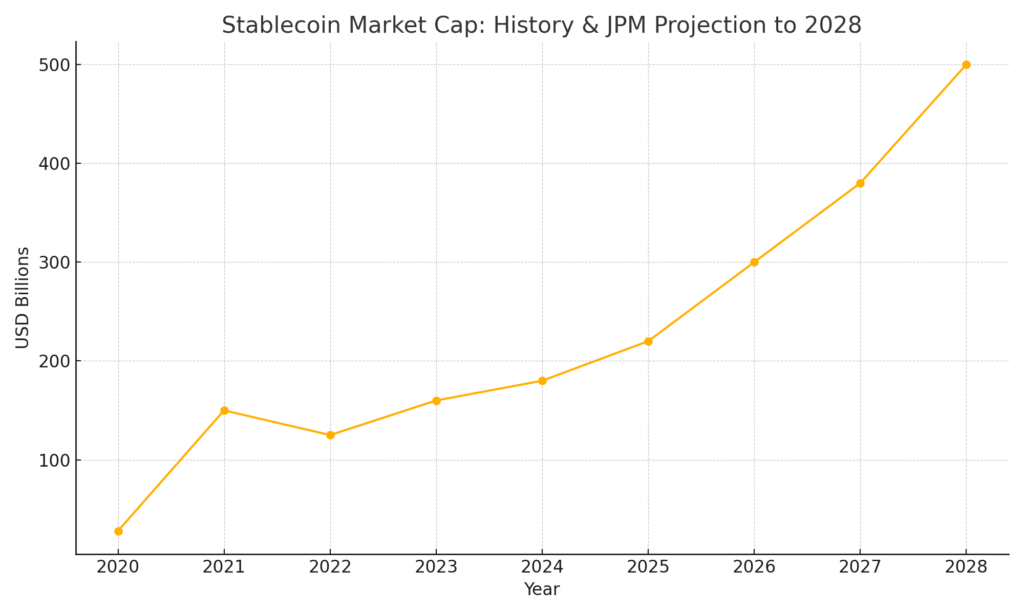

Jamie Dimon called Bitcoin a “fraud” years ago, threatening to fire traders who touched it. Yet his bank is now piloting deposit tokens, stablecoin rails, and crypto‑collateral lending. The contradiction is more optics than substance: Dimon still derides permissionless crypto, but he embraces regulated digital cash and tokenized assets—products that fit neatly inside banking charters and compliance regimes. The bank’s research desk places the stablecoin TAM at ~$500B by 2028, dismissing loftier $1T–$2T predictions as overenthusiastic.

3. A Broader Megabank Pattern: Citi, BofA, Goldman, Morgan Stanley

JPMorgan isn’t alone. In Q2 earnings calls and recent interviews:

- Citigroup is actively deploying Citi Token Services for cross‑border cash movements and is evaluating an in‑house stablecoin, though tokenized deposits remain priority one.

- Bank of America’s Brian Moynihan says a stablecoin play is ready to go once regulation is clearer.

- Goldman Sachs is researching but still “studying.” Morgan Stanley is evaluating, not launching.

The takeaway: the top six U.S. banks are converging on tokenized cash rails, but product velocity depends on regulatory certainty and client demand.

4. Why Crypto-Backed Loans Matter for Builders and Yield Seekers

Liquidity Without Liquidation: For hedge funds, corporates, DAOs, and family offices sitting on large BTC/ETH treasuries, a credit line means no forced selling during bull runs—or tax events.

Structured Products & Tokenized Credit: Expect structured lending notes, revolving credit facilities tied to on-chain collateral, and auction‑based margin call systems. Think “prime brokerage for crypto” but with Basel‑aligned risk buckets and on-chain verification points.

New Revenue Streams:

- Collateral Oracles & Monitoring: Tools that feed real‑time collateral health to both banks and borrowers.

- Tokenized Credit Lines: TradFi loans tokenized for DeFi liquidity pools—earning spread between bank prime rates and on-chain yields.

- Regulated Stablecoin Flows: Payments, B2B settlement, and yield products centered on bank‑issued stablecoins (lower counterparty risk vs. USDT/USDC for certain clients).

5. Risk, Regulation, and the Fine Print

The GENIUS Act (recent U.S. legislation) gives stablecoins federal oversight and bans yield‑bearing versions, pushing banks toward conservative, fully reserved models. If JPMorgan’s facility launches, expect:

- Haircuts & Volatility Buffers: BTC’s drawdowns >50% demand thick collateral cushions and intraday margining.

- Custody Constraints: Assets will likely sit with qualified custodians (possibly JPM’s own) under tri-party agreements.

- Oracle Risk & Liquidation Pathways: Banks need deterministic liquidation rails—centralized exchanges, RFQ networks, or regulated crypto prime brokers.

6. Strategic Plays for Startups and Protocols

A. Collateral Efficiency Tooling

- Automated LTV adjusters, cross‑chain rehypothecation trackers.

- Off‑chain/on‑chain data bridges for compliance (KYC/AML, Travel Rule) while preserving user privacy.

B. Tokenized Cash Management

- Treasury dashboards that optimize between bank stablecoins, deposit tokens, and public stablecoins based on yield, counterparty risk, and on/off‑ramp speed.

C. Real-World Payment Integrations

- Merchant acquiring with instant settlement in regulated stablecoins.

- Cross‑border B2B rails replacing SWIFT for certain corridors, using tokenized deposits.

D. Compliance-as-a-Service Layers

Banks will demand provable identity, source of funds, and transaction traceability. Startups that package Travel Rule payloads, AML screening, and reporting dashboards for both banks and crypto-native clients can sit in the flow of funds.

7. Competitive Landscape: DeFi Lenders vs. Banks

DeFi lenders (Aave, Maker, etc.) already provide crypto‑backed loans, but without USD prime-rate pricing, insured deposits, or traditional credit underwriting. JPMorgan can undercut DeFi rates for top-tier clients (thanks to their balance sheet) yet charge an “institutional convenience premium.” Conversely, DeFi can remain faster and composable. A hybrid model is likely: banks originate, DeFi diversifies risk—if legal wrappers permit.

8. Stablecoins: The Spine of the New Rails

McKinsey calls 2025 a tipping point for tokenized cash, urging incumbents to prepare or risk being disintermediated. JPMorgan’s conservative $500B forecast still implies >2.5x growth from today’s ~$180B market. The real question: how much of that will be bank‑issued versus crypto‑native stablecoins?

[Insert Figure 1: “Stablecoin Market Cap: History & JPM Projection to 2028” here]

The battle lines:

- Public Stablecoins (USDT/USDC) excel in crypto-native ecosystems.

- Bank Stablecoins/Deposit Tokens may dominate regulated B2B flows and corporate treasuries.

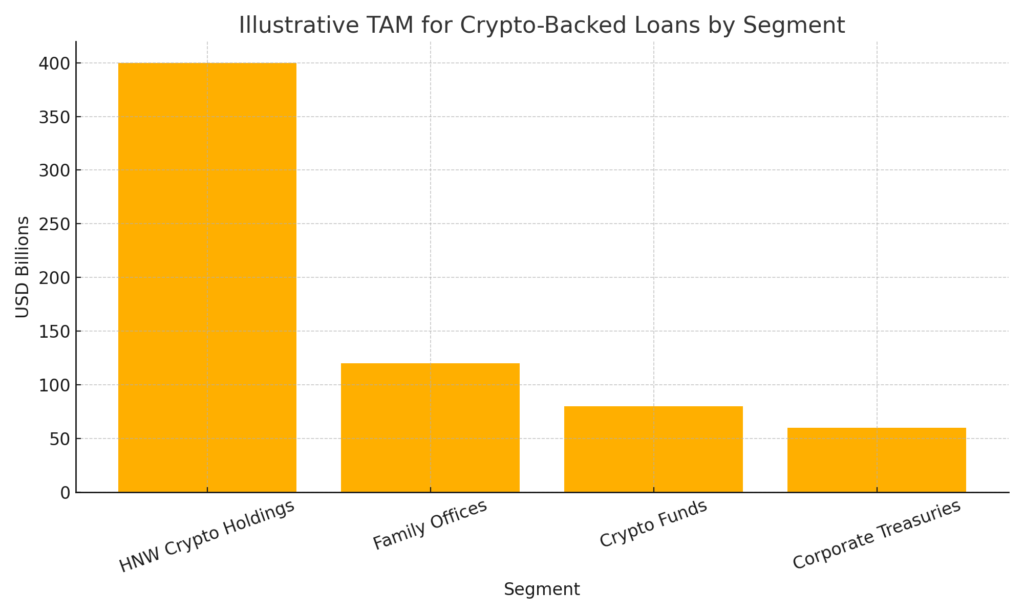

9. Total Addressable Market for Crypto-Collateral Lending

Consider HNW individuals, family offices, crypto funds, and corporate treasuries holding digital assets. Even a fraction pledging collateral could unlock a multi‑hundred‑billion market. (Illustrative segmentation below.)

[Insert Figure 2: “Illustrative TAM for Crypto-Backed Loans by Segment” here]

These numbers are directional—exact TAM depends on regulatory green lights, acceptable LTVs, and drawdown behavior during stress periods.

10. Actionable Next Steps for Readers

- Position for Collateral Onboarding: Build integrations with custodians, pricing oracles, legal docs automation (ISDAs/GMRA‑like for crypto).

- Design Yield Products Around Stablecoin Flows: Offer swap, hedging, and short‑term liquidity products to corporates converting between fiat, bank stablecoins, and public stablecoins.

- Leverage Tokenized Deposits: Explore programmable treasuries that time-lock funds, automate payables/receivables, or execute conditional payments.

- Compliance Layer Partnerships: Adopt Travel Rule and AML APIs early; banks will prefer plug‑and‑play partners.

- Scenario Plan for Regulation: The GENIUS Act may be first of many—prepare for restrictions on yield‑bearing stablecoins and privacy demands.

11. Conclusion: The Blurring Line Between TradFi and DeFi

JPMorgan’s potential crypto‑collateral loans symbolize an irreversible trend: traditional finance is not just “dipping toes” but building pipes to carry digital assets at scale. As regulation hardens and tokenized cash rises, the winners will be those who design products that respect banking rules while leveraging crypto’s programmability. For founders and investors chasing the next revenue stream, the opportunity isn’t just “number go up”—it’s in the infrastructure and services that make tokenized value usable, compliant, and liquid across both worlds.