Main Points :

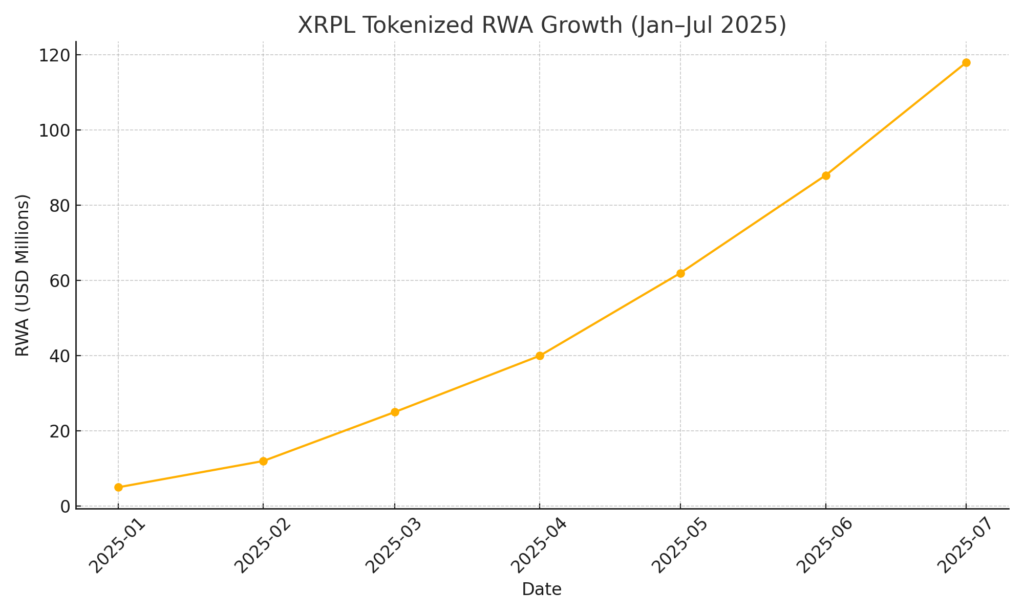

- XRPL’s tokenized real‑world assets (RWAs) jumped from $5M in January 2025 to over $118M in July 2025, a ~2,260% surge in six months.

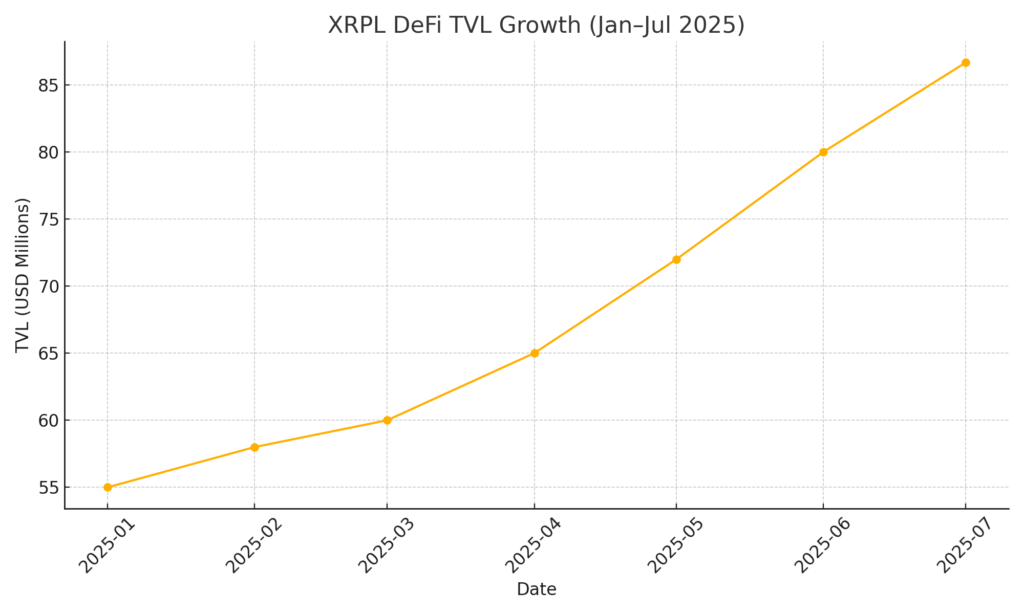

- DeFi total value locked (TVL) on XRPL climbed 57% to roughly $86.66M, signaling an institutional‑grade liquidity layer forming on low‑fee rails.

- Ripple’s compliance‑first USD stablecoin “RLUSD” received an “A” rating from Bluechip, eclipsing USDC (B+) and USDT (D).

- Ripple is pursuing a U.S. national bank charter and potential Federal Reserve master account access, aiming to fuse crypto-native infrastructure with core banking pipes.

- Global adoption is accelerating: UAE, Europe, APAC, and Latin America are onboarding XRPL for tokenization pilots—ranging from U.S. Treasuries to real estate deeds.

- Ondo Finance issued its short-term U.S. Treasury fund (OUSG) on XRPL, enabling 24/7 subscription/redemption via RLUSD.

- A strategic partnership with AEON could put RLUSD/XRP payments in 20 million Southeast Asian merchant locations, including brands like Uniqlo, McDonald’s, and Starbucks.

- The broader tokenization market is projected to swell from $600B in 2025 to ~$19T by 2033, and XRPL is positioning itself as a core settlement and compliance layer.

- For builders hunting the next revenue stream, opportunities span RWA market-making, compliance tooling, cross-border payment rails, and tokenized debt/real‑estate issuance services.

1. The Six-Month Blastoff: From $5M to $118M in Tokenized RWAs

XRPL’s RWA market didn’t just grow—it detonated. According to Ripple’s latest disclosures, the total value of tokenized real-world assets on XRPL expanded from $5 million in January 2025 to more than $118 million by July 2025, a ~2,260% increase. That’s not mere momentum; it’s a structural shift in how capital is beginning to view on-chain infrastructure. Traditional asset managers that once dipped toes are now rolling up their sleeves.

This explosive growth aligns with a broader macro trend: institutional appetite for tokenization as a way to unlock liquidity, reduce settlement friction, and enable fractional ownership. The early wave was dominated by U.S. Treasuries and real estate—stable, yield-bearing, and legally straightforward to securitize. XRPL’s characteristics—near-zero fees, deterministic finality, and production-grade reliability (330+ million transactions processed historically)—make it a logical venue for pilots graduating into production.

2. DeFi on XRPL Finds Its Institutional Groove

While XRPL is often framed as a payments rail, its DeFi layer has quietly sharpened its institutional edge. Total value locked in XRPL DeFi protocols surged 57% in recent months to around $86.66 million. That growth is modest compared to Ethereum giants, but the signal is clear: XRPL-native liquidity is forming, and it’s compliance-attuned. Protocol designers are integrating KYC-friendly gateways, permissioned pools, and audit-grade asset registries, anticipating the needs of banks and fund managers rather than anon farmers.

For builders, this creates a sandbox tailored to regulated yield strategies. Think: RLUSD‑denominated money markets, tokenized receivables, or permissioned liquidity pools for short-dated Treasuries. The arbitrage here isn’t just basis trades—it’s regulatory comfort, a commodity that commands a premium in 2025’s tightening oversight era.

3. Compliance as a Feature: RLUSD’s “A” Rating and Banking Ambitions

Ripple’s RLUSD stablecoin entered in 2025 with a bold thesis: win on transparency and regulation. Bluechip, a non-profit stablecoin rating body, gave RLUSD an “A” grade, surpassing USDC’s “B+” and USDT’s “D”. The architecture is simple but powerful: fully reserved, custodied by BNY Mellon, and designed to be audit-friendly. In a world where stablecoin scrutiny is intensifying, this compliance-first spirit differentiates RLUSD from yield-hunting but opaque rivals.

Ripple’s ambition doesn’t stop at tokens. On July 3, 2025, CEO Brad Garlinghouse announced Ripple had applied for a U.S. national bank charter. If granted, Ripple would operate under the Office of the Comptroller of the Currency (OCC), enabling:

- Direct access to Fed payment networks for instant settlement

- Potential FRB master account access, allowing RLUSD reserves to sit directly at the central bank

- A killer combination: crypto-native speed with banking-grade trust

For investors, this is a signpost: the line between fintech, crypto, and banking is dissolving. For startups, it means the bar is rising—any stablecoin or RWA platform without bank-grade compliance will feel pressure to level up or niche down.

4. Geography of Adoption: XRPL’s Global Footprint

Middle East (UAE): Ripple secured a Dubai Financial Services Authority license, opening doors to a $400B trade corridor. Collaborations with Zand Bank and Mamo Pay streamline cross-border remittances, and a real estate deed tokenization pilot with Ctrl Alt showcases how XRPL can handle legally sensitive registries.

Europe: Heavyweights like DZ Bank, DekaBank, and BBVA Switzerland are experimenting with XRPL for asset management and digital securities. A Société Générale subsidiary issued a euro-pegged stablecoin on XRPL, underlining that multiple fiat rails—not just USD—will coexist to support region-specific compliance and FX hedging.

Asia-Pacific: Partnerships with Straits (Singapore) and BDACS (Korea) are building the backbone for institutional digital asset infrastructure. Expect region-specific products: e.g., tokenized invoice factoring in Southeast Asia or yen‑denominated funds for Japanese institutions.

Latin America: Brazil’s crypto exchange Mercado Bitcoin plans to tokenize roughly $200M in assets on XRPL, pursuing local yield opportunities and 24/7 secondary trading. Meanwhile, UK-based Archax and asset manager abrdn are pushing XRPL-based digital securities, while Guggenheim Treasury Services eyes XRPL to streamline fund operations.

This mosaic illustrates a key insight: tokenization is hyper-local in regulation but global in infrastructure. The winners will be platforms that can adapt to local legal templates yet maintain a unified settlement backbone—exactly where XRPL seems to be positioning itself.

5. Ondo Finance, OUSG, and the 24/7 Treasury Market

One of the most instructive case studies is Ondo Finance deploying OUSG (a tokenized short-term U.S. Treasury fund) on XRPL. Investors can subscribe and redeem using RLUSD, with instant settlement and no banking hours. This configuration solves pain points for treasurers and DAOs alike:

- Intraday liquidity management without wire cut-off times

- Transparent NAV updates on-chain

- Reduced counterparty risk through segregated, audited reserves

This blueprint is replicable: tokenized credit funds, real estate income trusts, or even carbon credit pools could adopt similar mechanics, provided the legal wrappers are compliant. Builders should note: The tech is easy; the legal structuring is the moat.

6. Payments at Scale: AEON Partnership and 20 Million Merchants

On June 26, 2025, AEON announced a strategic partnership with Ripple to integrate XRP and RLUSD payments across 20 million Southeast Asian merchants, including household brands like Uniqlo, McDonald’s, and Starbucks. Through AEON Pay, users can spend RLUSD or XRP seamlessly at checkout.

This is more than “crypto payments are coming” hype. It’s a real distribution network, where settlement occurs on XRPL rails, fees are minimal, and FX can be handled via stablecoin swaps or automated market makers. Expect loyalty programs, cashback in RLUSD, and embedded finance primitives to ride on top of these rails.

For entrepreneurs, this opens doors to:

- POS-integrated DeFi yield accounts for merchants

- Stablecoin-based BNPL products

- Geo-fenced reward tokens tied to spend data

7. The $19 Trillion Horizon: Tokenization as Financial Bedrock

A Ripple–BCG report projects the tokenization market to scale from $600B (2025) to ~$19T by 2033. Whether the exact number hits or misses, the directional bet is clear: digitized claims on real assets will be standard. XRPL brings:

- Low-cost, high-speed settlement

- Battle-tested infrastructure

- Growing roster of regulated partners

But success will be unevenly distributed. Consider three axes of opportunity:

- Origination: Onboarding new asset classes (trade finance, equipment leases, music royalties) with compliant wrappers.

- Distribution: Building interfaces and liquidity venues that make these RWAs tradable and composable.

- Risk/Compliance Services: KYC, AML, travel rule, tax reporting, and audit trails as on-chain middleware.

8. Revenue Plays for Builders and Investors

If you’re scanning for the next income stream, isolate niches where regulatory friction meets on-chain efficiency:

- RWA Market-Making & Liquidity Bridging: Provide two-sided liquidity between RLUSD, EUR stablecoins, and tokenized bonds/notes. Spread capture + compliance premium = juicy margins.

- Compliance Middleware: Travel rule adapters, KYB onboarding for RWA issuers, and on-chain attestations.

- Cross-Border Payroll & Treasury Ops: SMEs need stable FX rails; embed RLUSD payouts with auto-hedging.

- Tokenized Real Estate Platforms: Focus on fragmented markets (e.g., Southeast Asian condos or Brazilian agricultural land) where legal structuring is complex but potential returns are high.

- Data Oracles & Valuation Feeds: Real-time NAV, interest accrual, or property appraisal oracles—sold as SaaS to issuers.

- Stablecoin FX “Primes”: RLUSD ↔ other regulated stables as an always-on FX corridor; fee each hop.

9. Risks and Execution Realities

Let’s stay sober:

- Regulatory whiplash: A single policy shift (e.g., stricter stablecoin reserve rules) can reshape business models overnight. Stay modular.

- Legal enforceability: Tokenized claims must map cleanly to real-world rights. Sloppy structuring = lawsuits.

- Liquidity fragmentation: Multi-chain RWA issuance could scatter liquidity; bridges and cross-chain AMMs must be bulletproof.

- Operational security: RWA smart contracts, oracles, and custodial partners are high-value targets. Defense-in-depth is non-negotiable.

10. Conclusion: XRPL as a Pragmatic Layer for Institutional DeFi

XRPL’s past six months weren’t a hype cycle—they were a product-market fit signal. From RWA issuance and DeFi TVL growth to a top-rated stablecoin and banking ambitions, every datapoint points to the same thesis: finance is moving on-chain, and compliance-first chains will capture the lion’s share of institutional flow.

Ripple’s pursuit of a bank charter, RLUSD’s A-grade rating, and real deployments across UAE, Europe, APAC, and Latin America collectively indicate that XRPL is no longer just a payments ledger—it’s a maturing financial substrate.

For participants looking for the next crypto-native revenue frontier, the path is practical, not speculative: tokenize real assets, build the compliance rails, and serve the merchants and treasurers who need 24/7, low-cost, trust-minimized finance. The tokenized reality is here—XRPL just gave it momentum.