Main Points:

- Former President Trump is preparing an executive order to allow cryptocurrencies, gold, and private equity in U.S. 401(k) retirement plans.

- The $9 trillion U.S. retirement market could see hundreds of billions of dollars flow into alternative asset classes.

- The order instructs federal regulators to identify and remove legal and procedural barriers to such investments.

- The Department of Labor has already revoked the 2022 guidance that discouraged crypto in retirement plans.

- Major private capital firms—Blackstone, Apollo, BlackRock—stand to benefit from expanded access to 401(k) savings.

- Critics warn of higher fees, limited liquidity, and valuation challenges compared to traditional mutual funds.

- This move signals a broader push to mainstream digital assets and deregulate U.S. financial markets.

Background: A Radical Shift for Retirement Savings

On July 18, 2025, the Financial Times reported that former President Donald Trump is poised to sign an executive order opening up the $9 trillion U.S. retirement market to alternative assets such as cryptocurrencies, gold, and private equity. If enacted this week, the order would mark a historic expansion of investment options within 401(k) plans, which have traditionally been limited to stock and bond mutual funds managed by plan providers.

The directive will instruct agencies like the Department of Labor (DOL), the Securities and Exchange Commission (SEC), and the Treasury Department to investigate the remaining legal, regulatory, and operational barriers preventing alternative investments from being offered in qualified retirement plans. It also calls for consideration of “safe harbor” provisions to protect plan fiduciaries from liability when they include these new asset classes.

Policy Mechanism: Removing the Roadblocks

Under the proposed executive order, federal regulators must:

- Identify Remaining Barriers – Pinpoint any statutory, regulatory, or interpretive hurdles that prevent plan sponsors from offering cryptocurrencies, precious metals, private equity, infrastructure funds, and other non‑traditional assets in 401(k) plans.

- Recommend Safe Harbors – Develop guidelines or safe‑harbor provisions that limit fiduciary liability for plan administrators who include these assets, thus assuaging fears of legal exposure.

- Promote Neutrality – Ensure future guidance adopts a neutral stance toward new asset classes, reversing the “extreme prudence” standard of the 2022 compliance guidance issued under the Biden administration.

On May 28, 2025, the DOL formally withdrew the 2022 guidance that had required plan fiduciaries to exercise “extreme care” before adding crypto options to retirement plans, signaling a shift toward a more permissive regulatory environment. The new executive order will cement this deregulatory trend, potentially fast‑tracking product development by financial firms eager to capture retirement‑plan allocations.

Market Impact: Hundreds of Billions at Stake

Allowing even a modest allocation—say 1 percent—to cryptocurrencies in 401(k) plans could inject roughly $90 billion into digital‑asset markets alone. And if plan sponsors allocate similar small percentages to private equity and real assets, total flows into alternative investments could reach several hundred billion dollars annually.

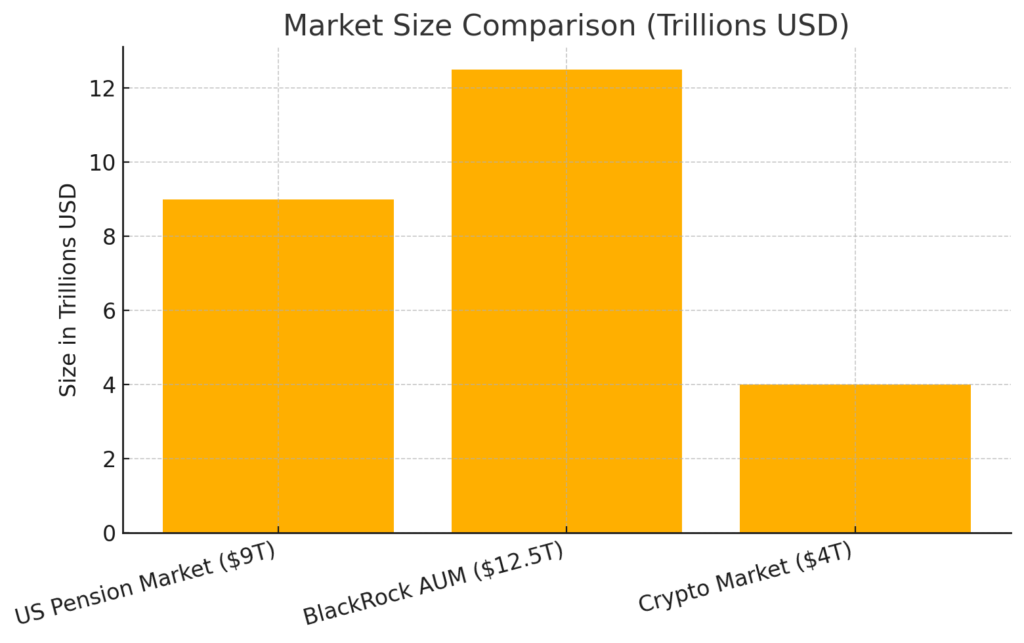

Figure: Market Size Comparison (in trillions USD)

Refer to the chart above for a visual comparison of the U.S. pension market ($9 T), BlackRock’s assets under management ($12.5 T), and the total crypto market ($4 T).

Benefits for Private Capital and Asset Managers

Major private-capital firms are already positioning themselves for this opportunity:

- Blackstone and Apollo have launched initiatives targeting 401(k) plan aggregators, aiming to integrate their private equity vehicles into retirement portfolios.

- BlackRock, with $12.5 trillion in assets under management, has signaled its interest in capturing pension flows for its iShares and private markets offerings.

These firms anticipate that expanded 401(k) access will become a cornerstone of their growth strategies, as they build out product suites—ranging from tokenized real estate funds to cryptocurrency ETFs—to meet plan‑sponsor demand.

Criticisms and Risks

Despite the potential upside, critics caution that alternative‑asset inclusion raises several concerns:

- Higher Fees – Private equity and hedge‑fund‑style products typically command management fees and performance fees far above those of index funds.

- Liquidity Constraints – Many alternative investments have lock‑up periods or limited redemption windows, incompatible with the daily valuation cycles of 401(k) plans.

- Valuation Transparency – Unlike publicly traded stocks and bonds, cryptocurrencies and private investments can lack standardized pricing, complicating plan accounting and compliance.

Financial commentators have warned that plan participants may assume a false sense of security, unaware of the distinct risk profiles and fee structures of these new assets.

Broader Implications for Crypto Adoption

This executive order is part of a larger push by the Trump administration to normalize and legitimize cryptocurrency in the U.S. financial system. Trump has frequently credited digital assets with energizing his political base and contributing to his 2024 electoral success. His prior actions include rescinding certain SEC enforcement actions and instructing the Treasury to consider regulatory frameworks that foster innovation in the digital‑asset ecosystem.

By embedding crypto into retirement‑savings vehicles—arguably the cornerstone of long‑term household wealth—the order could accelerate mainstream adoption, driving greater institutional involvement, market liquidity, and service‑provider innovation.

Conclusion

If signed, the proposed executive order represents a monumental shift in U.S. retirement‑plan policy, unlocking a $9 trillion market to a new generation of alternative investments. While the move promises fresh sources of yield and diversification for plan participants—and vast growth opportunities for private‑capital firms—it also introduces novel risks around fees, liquidity, and valuation. As regulators work to carve out safe‑harbor rules and remove procedural roadblocks, the financial industry must balance innovation with investor protection to ensure that this landmark policy change delivers sustainable benefits for American workers.