Main Points:

- Circle filed for a national trust bank charter with the U.S. Office of the Comptroller of the Currency (OCC) just one month after its blockbuster IPO.

- Approval would enable Circle to custody its own USDC reserves, issue and manage tokenized assets, and offer institutional custody services under federal oversight.

- The move anticipates forthcoming U.S. stablecoin regulation (the GENIUS and CLARITY Acts) and positions Circle to lead evolving industry standards.

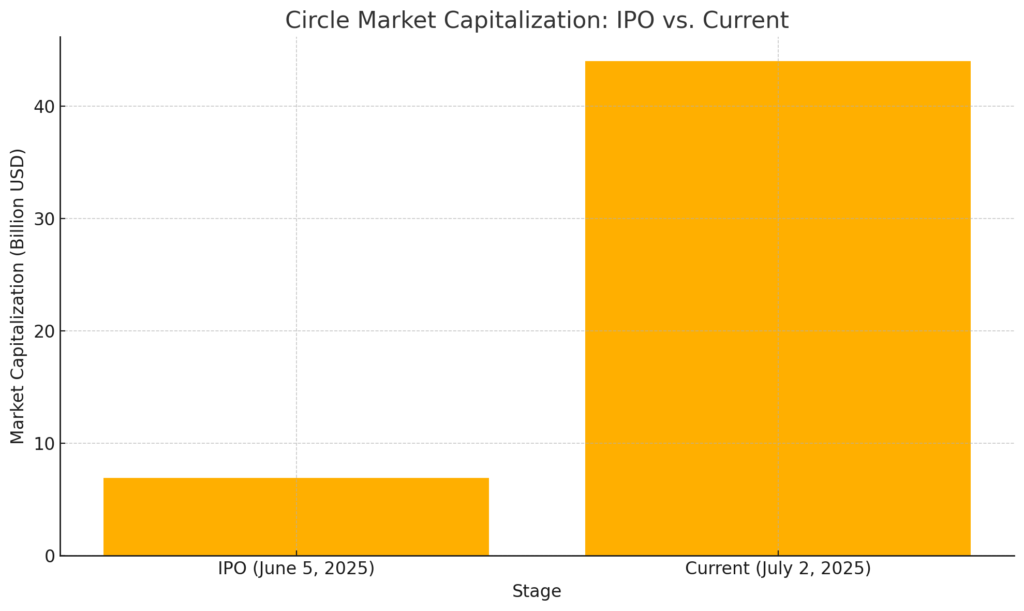

- Circle’s market capitalization has soared from roughly $6.9 billion at IPO to about $44 billion as of July 2, 2025.

- Broader adoption of USDC by platforms like Shopify and Worldcoin underscores practical demand for regulated stablecoins.

Strategic Shift: From IPO to National Trust Bank Application

Circle Internet Group, issuer of the USDC stablecoin, dramatically bolstered its regulatory credentials by filing an application for a national trust bank charter with the OCC on June 30, 2025, only a month after its New York Stock Exchange debut on June 5 (IPO market cap ~$6.9 billion). The proposed entity, First National Digital Currency Bank, N.A., would be empowered to act as a federally regulated trust institution—distinctly focused on custody rather than traditional deposit-taking or lending activities.

Under this charter, Circle would transition USDC reserve management in-house, no longer relying solely on third parties such as BlackRock or BNY Mellon for safeguarding its cash and short-dated U.S. Treasury collateral. While Circle plans to retain some delegation to leading financial institutions, direct OCC oversight promises enhanced transparency and governance—core tenets espoused by CEO Jeremy Allaire as vital to sustaining institutional trust and compliance in digital asset markets.

Bolstering Compliance Ahead of U.S. Stablecoin Regulation

The trust bank application is a calculated preemptive move in light of advancing bipartisan stablecoin legislation in Washington. The recent Senate-passed GENIUS Act, combined with the House’s pending CLARITY Act, is poised to mandate clear reserve backing, monthly attestation requirements, and explicit definitions distinguishing stablecoins from securities. By securing a federal charter, Circle aims to meet or exceed anticipated regulatory obligations—thereby setting a de facto industry benchmark and potentially influencing rule-making outcomes.

Institutional players and retail giants are already experimenting with USDC. Shopify recently integrated stablecoin payouts, and Worldcoin’s World App adopted USDC on its World Chain blockchain for user transactions. These practical deployments illustrate growing real-world demand for a trusted, regulated digital dollar alternative—one that a chartered Circle bank would underpin with direct custody and governance mechanisms.

Market Response and Valuation Surge

Circle’s IPO was initially underpriced at $31 but closed its first trading day near $83.23, signaling robust demand underpinned by confidence in its regulatory posture and USDC’s market prominence. Since then, the stock climbed to a peak of $298.99—translating to a market cap of approximately $44 billion by July 2, 2025 (Figure 1).

Analyst projections have been bullish: Barclays, Bernstein, and Canaccord set price targets above $200, reflecting optimism about USDC expansion and Circle’s institutional partnerships. However, cautionary notes from JPMorgan and Goldman Sachs highlight potential overvaluation and speculative momentum following the rapid post-IPO surge. Nonetheless, Circle’s decisive regulatory strategy and growing ecosystem support suggest these valuations may be underpinned by substantive business developments rather than mere hype.

Comparative Context: Anchorage Digital and Industry Peers

If approved, Circle would become only the second crypto-native entity to hold a national trust charter, following Anchorage Digital Bank’s pioneering clearance in January 2021. Unlike Anchorage, which offers both custody and financing services, Circle’s planned bank would eschew traditional deposit and lending functions, focusing exclusively on:

- USDC Reserve Custody

- Institutional Digital Asset Custody (tokenized securities, bonds)

- Issuance and Management of Tokenized Assets

This narrower scope underscores Circle’s intent to maintain operational simplicity while maximizing trust and compliance. By contrast, emerging crypto banks—like TBD by Kraken—are exploring broader full-service offerings. Circle’s specialized model may appeal particularly to institutional clients seeking transparent, regulatory-aligned custody solutions without the complexity of credit risk.

Practical Implications for Blockchain Applications

Institutional adoption of USDC custody services via a federally chartered entity could unlock new blockchain-based financial products, such as:

- Programmable Asset Issuance: Tokenized bonds or equities with on-chain settlement.

- Cross-Border Payments: Faster, cheaper dollar-denominated transfers.

- Decentralized Finance (DeFi) Integration: Enhanced liquidity in protocols requiring regulated collateral.

These use cases resonate with enterprises and developers targeting pragmatic blockchain implementations. A trust charter enhances legal certainty, mitigates counterparty risk, and streamlines compliance—critical factors for widespread enterprise uptake.

Future Outlook and Industry Leadership

Circle’s bank application, in concert with its IPO, positions the firm at the vanguard of digital asset finance—bridging DeFi innovation with traditional regulatory frameworks. Pending OCC approval, Circle is likely to shape emerging norms for stablecoin issuance and custody under federal law. This could catalyze a broader industry shift, compelling competitors to pursue similar charters or enhance transparency to maintain market credibility.

Moreover, as federal stablecoin legislation becomes law—potentially within the next 12 months under the GENIUS and CLARITY Acts—Circle’s fortified infrastructure and compliance-first culture may deliver a sustainable competitive advantage, particularly among institutional users wary of regulatory gaps.

Conclusion

Circle’s swift transition from a successful IPO to a trust bank application underscores the company’s commitment to regulatory leadership and institutional trust. By internalizing USDC reserve custody and embracing federal oversight, Circle aims to set a new standard for stablecoin governance. As U.S. stablecoin regulation crystallizes, Circle’s strategic foresight and expanding ecosystem partnerships—from Shopify to Worldcoin—suggest that USDC will continue to play a central role in blockchain’s practical adoption. Institutional demand for transparent, compliant digital dollar solutions is mounting, and Circle’s national trust bank could become the fulcrum of a next-generation digital asset financial system.