Main Points:

- Circle filed for a national trust bank charter (“First National Digital Currency Bank”) with the U.S. Office of the Comptroller of the Currency (OCC) to self-custody USDC reserves and offer institutional custody services.

- The charter focuses solely on digital asset custody; deposit-taking and lending remain off-limits.

- If approved, Circle would shift USDC reserves from BNY Mellon/BlackRock to its own federally regulated entity.

- The move strengthens Circle’s governance post-IPO and aligns with anticipated federal stablecoin regulations under the GENIUS Act.

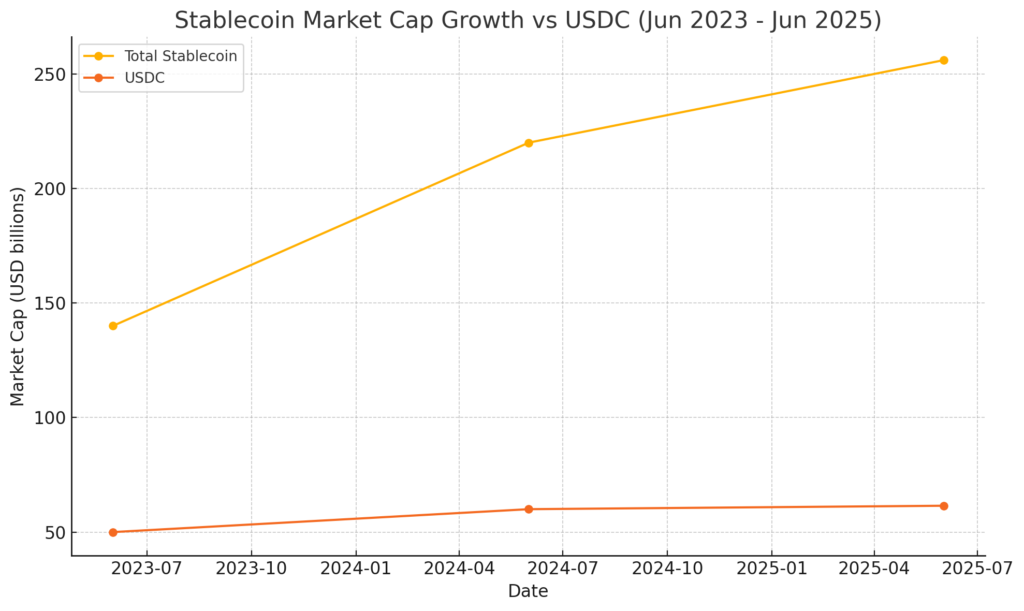

- Total stablecoin market cap has surged from around $140 billion in June 2023 to $256 billion in June 2025, with USDC growing from $50 billion to $61.5 billion over the same period.

- A robust U.S. regulatory framework for stablecoins is imminent: the Senate passed the GENIUS Act on June 17, 2025, requiring issuers to maintain liquid-asset backing and publish monthly disclosures.

- This charter would position Circle ahead of peers like Tether amid tougher disclosure rules, and complement institutional demand for transparent, bank-regulated stablecoin infrastructure.

Background: Circle’s OCC Filing

On June 30, 2025, Circle Internet Financial disclosed its application to the U.S. Office of the Comptroller of the Currency (OCC) to establish the “First National Digital Currency Bank, N.A.” This federally chartered trust bank would focus exclusively on custodial services for digital assets, marking a significant evolution from traditional banking activities. If approved, Circle would become one of only two crypto firms—with Anchorage Digital being the other—to hold a national trust bank charter, underscoring the pioneering nature of this move.

Motivation for a Bank Charter

Circle CEO Jeremy Allaire emphasized that pursuing a trust bank charter is a logical extension of Circle’s commitment to “the highest standards of trust and transparency,” especially in the wake of its blockbuster IPO that valued the company near $18 billion. By self-custodying USDC reserves, Circle aims to:

- Eliminate Third-Party Custody Risks: Transitioning reserve management from BNY Mellon and BlackRock to an OCC-regulated entity.

- Enhance Institutional Confidence: Providing banks, insurers, and asset managers with a regulated on-ramp to USDC.

- Streamline Governance: Aligning its corporate structure with its public-market obligations and evolving regulatory expectations.

USDC Reserve Management Shift

Currently, USDC reserves—comprised of U.S. dollar cash and short-term U.S. Treasuries—are held at BNY Mellon and managed by BlackRock. Under First National Digital Currency Bank, Circle would take direct control of these assets, enabling real-time reserve audits and more agile treasury operations. This structural change could reduce counterparty risk and improve reserve yield optimization, potentially increasing USDC yield for institutional partners.

Regulatory Landscape: The GENIUS Act

Stablecoin issuance in the U.S. has lacked a unified federal framework—until now. On June 17, 2025, the U.S. Senate passed the “Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act” by a 68–30 margin. Key provisions include:

- Permitted Issuers: Only banks and approved fintech firms may mint payment stablecoins.

- Reserve Backing: 100% of outstanding coins must be backed by liquid assets (cash, Treasuries).

- Disclosure Requirements: Monthly publication of reserve composition and proof of reserves.

- Enforcement Powers: The OCC, Federal Reserve, and FDIC may impose penalties for non-compliance.

President Trump is expected to sign the reconciled legislation before the end of summer, ushering in a new era of institutional-grade stablecoin issuance.

Industry Implications and Competitive Dynamics

Tether vs. USDC

Tether (USDT), with a $156 billion circulating supply, faces increased scrutiny under the GENIUS Act due to its historically opaque reserve practices—investments in Bitcoin and precious metals among them. In contrast, USDC’s fully liquid reserve model positions Circle to benefit from regulatory clarity, potentially eroding USDT’s U.S. market share.

Institutional Services Expansion

The new trust bank would permit Circle to offer custody services for tokenized assets beyond USDC, such as tokenized Treasuries or other dollar-pegged tokens. This service aligns with a pivot by banks and wealth managers toward digital asset custody under regulated frameworks.

Market Cap Growth Trends

The stablecoin sector has experienced meteoric growth, from $140 billion in June 2023 to $256 billion by June 2025, while USDC’s share expanded from $50 billion to $61.5 billion. (See the chart above.) This trajectory highlights the growing appetite for programmable money and on-chain liquidity among institutional actors.

Future Outlook

- Approval Timeline: OCC charter applications typically take 12–18 months; market participants will watch for conditional approvals similar to Anchorage Digital’s 2021 application.

- Yield Strategies: With direct reserve control, Circle could enhance USDC yields via optimized Treasury allocations or repurchase agreements.

- Product Innovation: The trust bank could facilitate on-chain repo markets, tokenized deposits, and cross-border payment rails using USDC as settlement currency.

- Global Expansion: A U.S. charter may serve as a blueprint for Circle’s regulatory engagement in Europe and Asia, accelerating the adoption of regulated digital currency banks worldwide.

Conclusion

Circle’s application to form the First National Digital Currency Bank represents a turning point for stablecoins and digital asset infrastructure. By internalizing reserve custody under an OCC charter, Circle is not only bolstering trust and transparency but also positioning USDC—and by extension, itself—at the vanguard of a maturing institutional market. With the GENIUS Act poised to codify these standards into law, traditional finance and crypto converge on a regulated, interoperable foundation. For investors and developers exploring new revenue sources, programmable money, and practical blockchain applications, Circle’s trust bank charter may well signal the next frontier in digital finance.