Main Points:

- Overall crypto market cap rose ~3% to $3.27 trillion in H1 2025.

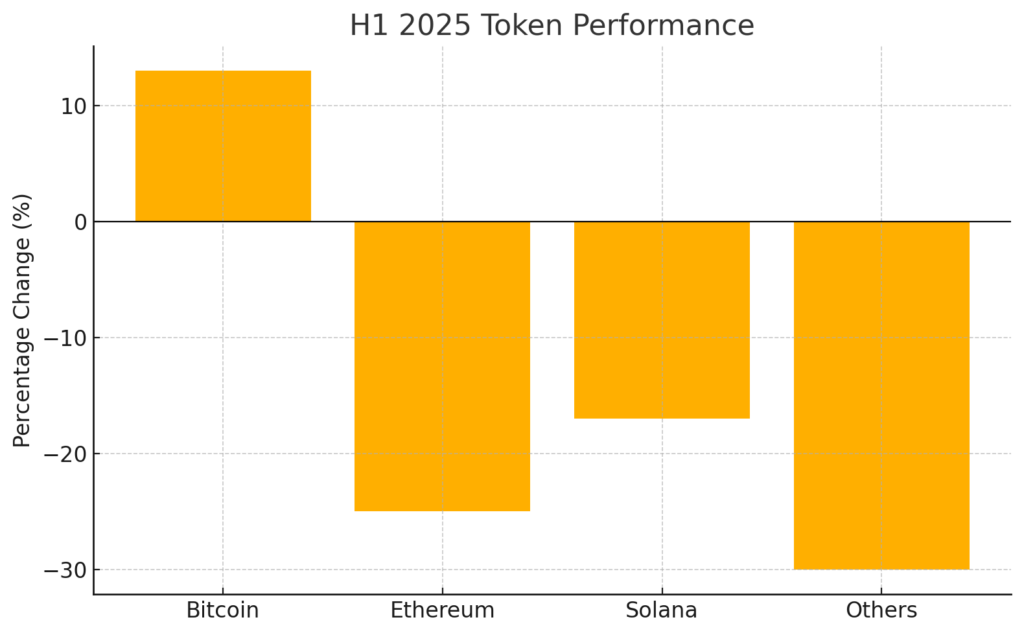

- Bitcoin outperformed with a 13% gain; Ethereum and Solana fell 25% and 17%, respectively.

- Smaller tokens (“Others”) plunged ~30%.

- Historical patterns suggest July strength, but Q3 often weaker for Bitcoin.

- Institutional demand—especially stablecoin issuers—has driven record Treasury purchases.

- Regulatory clarity (MiCA in EU; GENIUS Act in US) setting stage for mainstream adoption.

- Continued corporate accumulation beyond Bitcoin, including Ethereum strategies.

Market Overview: H1 2025 Performance

Despite global economic headwinds—rising tariffs, recession fears, geopolitical conflicts, and U.S. political uncertainty—the total crypto market cap edged up a modest 3% in the first half of 2025, from $3.18 trillion to $3.27 trillion by June 30, 2025 (1 USD = ¥144) (Source: original article). This stability hides a deeply skewed performance: benchmarks measured by TradingView show that assets outside the top 10 (“Others” index) tanked by 30%, underscoring risk-off sentiment among smaller tokens.

Token-by-Token Breakdown

- Bitcoin (BTC): Up ~13%, continuing its role as market anchor during periods of uncertainty and fund rotations.

- Ethereum (ETH): Down ~25%, pressured by slower-than-expected DeFi flows and high on-chain fees.

- Solana (SOL): Declined ~17% after network outages undermined confidence in its throughput reliability.

- Others: The “OTHERS” index (ex-top-10) plunged 30%, reflecting steep sell-offs in niche and low-liquidity tokens.

<div><!– Chart rendered above –></div>

Historical Patterns: July Strength vs. Q3 Risks

Historically, July has been a strong month for crypto. LMAX Group’s Joel Kruger notes that since 2013, July has averaged a 7.56% return for major crypto indices. This coincides with easing summer volatility and fund portfolio rebalancing. However, the transition into Q3—starting in July—has often marked Bitcoin’s weakest quarterly stretch; Bitfinex analysts warn the July–September period has averaged only a 6% gain since 2013, making it “historically the weakest time” for BTC (Bitfinex report, June 30, 2025).

Institutional Adoption: Beyond Bitcoin

Corporate and institutional strategies are expanding beyond Bitcoin into diversified digital assets. Coinbase Institutional highlights growing treasury diversification: firms are announcing Ethereum accumulation plans alongside BTC reserves. Meanwhile, trading desks report that stablecoin issuers now hold over $200 billion in U.S. Treasuries—as collateral to maintain 1:1 pegs—a figure set to rise with stablecoin market cap growth (currently $256 billion, up from $180 billion in January). Each $10 billion increase in stablecoin supply typically translates into $10 billion in T-bill purchases, bolstering short-term Treasury demand.

Regulatory Developments: Laying the Foundation

- EU’s MiCA Regulation: Fully applicable since December 30, 2024, MiCA standardizes issuer capital, reserve, and disclosure requirements for stablecoins and other tokens, reducing fragmentation across EU member states.

- U.S. GENIUS Stablecoin Act: Passed Senate June 2025; mandates audited reserves and strict AML/KYC protocols. This could reshape market share—Circle’s USDC may benefit, while Tether (USDT, $156 billion cap) faces compliance hurdles.

- BIS Warning: The Bank for International Settlements warns stablecoins risk financial stability and monetary sovereignty if unregulated, urging central banks and private sector collaboration for resilient tokenization infrastructures.

Practical Implications for Investors and Developers

- Portfolio Adjustment

- Consider overweighting Bitcoin given historical July strength and H1 resilience.

- Evaluate selective altcoin exposure; prioritize projects with real-world use cases (DeFi, layer-2 scaling).

- Stablecoin Strategies

- Leverage regulated stablecoins for low-slippage on-chain operations.

- Monitor reserve disclosures under MiCA/GENIUS frameworks to mitigate issuer risk.

- Institutional Services

- Expect expanded custody and treasury services integrating tokenized assets.

- DeFi protocols may see increased institutional staking and liquidity provision under clearer regulation.

- Blockchain Utilization

- Enterprises should explore tokenization of real-world assets, guided by evolving regulatory clarity.

- Cross-border payments leveraging stablecoins can reduce settlement times and FX costs.

Conclusion

The first half of 2025 showcased a bifurcated crypto market: Bitcoin’s steady ascent contrasting sharply with declines across Ethereum, Solana, and smaller tokens. As we head into H2, historical patterns and institutional dynamics suggest potential upside, tempered by typical Q3 headwinds. Regulatory milestones—MiCA in the EU, the GENIUS Act in the U.S.—are setting robust guardrails, paving the way for broader enterprise adoption and stablecoin-driven liquidity in traditional markets. For investors and developers, the path forward lies in balancing Bitcoin exposure, leveraging stablecoin efficiency, and building applications that capitalize on a maturing regulatory landscape.