Main Points:

- FHFA director William Pulte directs Fannie Mae and Freddie Mac to prepare proposals for counting cryptocurrency holdings as assets in mortgage assessments.

- The decision aligns with President Trump’s agenda to make the U.S. a global cryptocurrency hub.

- Historically, crypto has been excluded due to volatility and regulatory uncertainty, despite pilot services like Figure’s crypto-backed loans.

- Potential benefits include expanded borrowing capacity, broader asset recognition, and deeper integration of digital assets into traditional finance.

- Key challenges involve asset valuation methodologies, volatility risk management, regulatory compliance, and exchange custody requirements.

- Industry reaction spans from enthusiastic support by crypto advocates to caution from risk officers and regulators.

- Future outlook suggests pilot programs, refined guidelines, and possible extension to other digital assets like stablecoins and tokenized real-world assets.

1. Introduction

On June 26, 2025, FHFA Director William J. Pulte ordered Fannie Mae and Freddie Mac to draft proposals for treating cryptocurrency holdings as bona fide assets in mortgage underwriting. This watershed directive marks the first time the government’s mortgage guarantors have been explicitly instructed to integrate digital assets into credit-risk evaluations. The move is billed as part of a broader effort—championed by President Trump—to position the United States at the forefront of global cryptocurrency adoption.

2. Historical Context of Crypto-Backed Lending

Prior to this announcement, lenders have largely excluded virtual currencies from mortgage‐asset calculations due to:

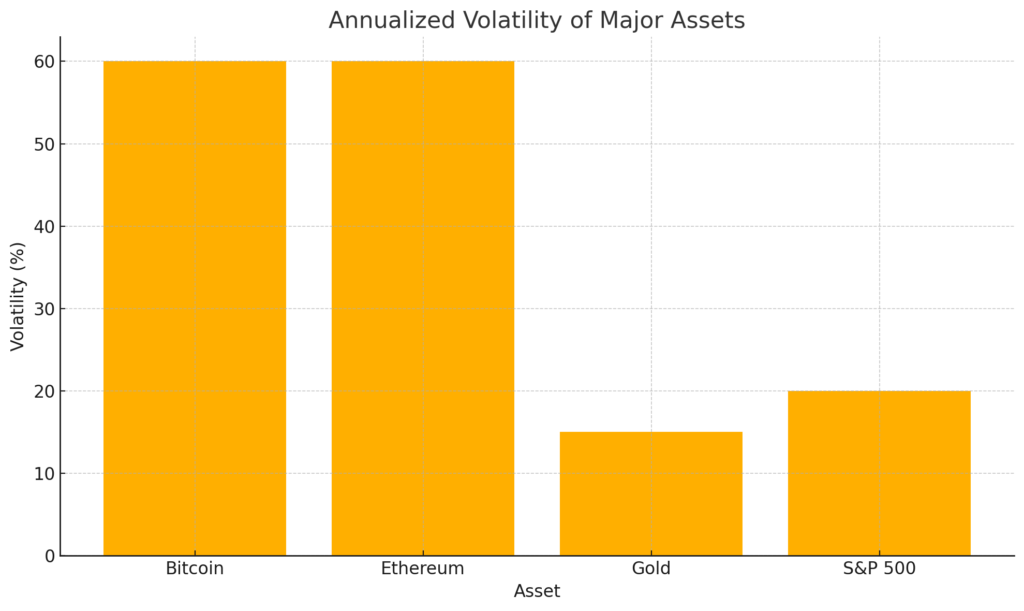

- Price Volatility: Bitcoin’s annualized volatility often exceeds 60%, dwarfing gold’s ~15% and the S&P 500’s ~20%, as illustrated below.

- Regulation Uncertainty: No consistent framework existed to verify custody, provenance, or exchange solvency.

- Limited Precedents: Figure, a fintech lender, launched crypto-backed mortgages in 2022, accepting BTC and ETH as collateral—but on a small scale.

This chart compares annualized volatility of major assets, underscoring the risk profile lenders must manage:

3. The FHFA Directive: Scope and Requirements

Director Pulte’s order carries several key stipulations:

- Eligible Assets: Only cryptocurrencies stored on U.S.-regulated centralized exchanges will be considered, ensuring AML/KYC compliance and custodial safeguards.

- Valuation Methodologies: GSEs must develop transparent models for daily pricing, haircuts, and volatility buffers to convert crypto valuations into USD reserves.

- Board Approval: Any final underwriting guideline revisions require sign-off by each entity’s Board of Directors before FHFA review.

- Timeline: While no formal deadline was publicly announced, industry observers expect initial proposals by Q4 2025.

4. Potential Benefits for Borrowers and Lenders

- Expanded Borrower Pools

- Crypto holders—often younger, high-net-worth individuals—will gain access to mortgage products without liquidating positions.

- Broader Asset Recognition

- Recognizing digital assets creates a more holistic financial profile, potentially reducing loan-to-value ratios and interest spreads.

- Market Liquidity and Innovation

- Encourages digital-asset investors to engage in real estate markets, fostering innovation in asset-backed lending.

- Competitive Differentiation

- Banks and fintechs that build robust crypto underwriting solutions may capture underserved segments and drive new product lines.

5. Risks and Implementation Challenges

- Price Fluctuations: Crypto prices can swing >10% in a single day; lenders must determine adequate haircut levels (e.g., 25–50%).

- Custody & Security: Dependence on regulated exchanges introduces counterparty risk; insurance and proof-of-reserves will be critical.

- Regulatory Landscape: Ongoing debates over SEC vs. CFTC jurisdiction, plus state-level money transmitter requirements, could complicate standardized guidelines.

- Operational Complexity: Integrating real-time pricing feeds, margin‐call triggers, and liquidation workflows will require significant tech investments.

6. Industry and Market Reactions

- Crypto Advocates: Michael Saylor (MicroStrategy) publicly pitched his firm’s Bitcoin credit model to FHFA and touted the move as “the next frontier in wealth integration”.

- Fintech Innovators: Figure and BlockFi have prepared pilot programs to share data on secured lending performance, aiming to demonstrate default rates under 1%.

- Traditional Lenders: Banks express guarded optimism, citing the need for rigorous stress-testing before adopting crypto collateral.

- Regulators: Some CFPB officials caution that consumer protections must keep pace, notably around margin calls and forced liquidations in down markets.

7. Broader Trends in Digital Asset Collateralization

- Stablecoins as Collateral: Emerging protocols are exploring USDC and Tether for lower-volatility asset pledges in consumer and commercial lending.

- Tokenized Real-World Assets: Platforms like Centrifuge are tokenizing invoices and real estate fractions—an adjacent frontier that could converge with crypto-backed mortgages.

- Institutional Adoption: Major banks (e.g., JPMorgan, Standard Chartered) are testing blockchain-based collateral management systems, signaling broader institutional comfort.

8. Future Outlook

- Pilot Launches (Late 2025–Early 2026)

- Expect small-scale mortgage offerings through partner banks, likely capped at 25% LTV on crypto collateral.

- Guideline Finalization

- FHFA and GSE boards will codify acceptable crypto types, haircut ranges, and custodial standards.

- Regulatory Harmonization

- Collaboration with SEC, CFTC, and state regulators will shape uniform custody rules and investor protections.

- Market Expansion

- If pilots succeed, broader consumer adoption could follow—potentially extending to multifamily lending and home equity lines.

9. Conclusion

The FHFA’s directive represents a landmark moment in bridging decentralized finance (DeFi) and traditional housing finance. By mandating Fannie Mae and Freddie Mac to evaluate cryptocurrency holdings as part of mortgage asset calculations, the agency is effectively expanding the spectrum of acceptable collateral and acknowledging the maturing role of digital assets in wealth portfolios. While significant challenges remain—particularly around volatility management, regulatory alignment, and operational readiness—the initiative has the potential to unlock new homeownership opportunities and catalyze innovation at the intersection of blockchain and real estate finance. As pilot programs roll out and guidelines crystallize, the next 12–18 months will be critical in determining whether this visionary step can translate into sustainable, consumer-friendly mortgage products.