Main Points:

- FHFA to study whether crypto holdings qualify in mortgage applications

- SEC’s repeal of SAB 121 paves way for institutional crypto integration

- Existing crypto‐backed mortgage products offered by specialized fintech firms

- Growing trend of borrowers using crypto profits to service home loans

- Potential policy implications and risk considerations for lenders and borrowers

- Forecasted emergence of mainstream banks offering crypto‐collateralized loans

Introduction

The U.S. Federal Housing Finance Agency (FHFA), which sets the rules for Fannie Mae and Freddie Mac, announced on June 24, 2025 that it will “study the usage of cryptocurrency holdings as it relates to qualifying for mortgages.” This pioneering move signals a possible expansion of the underwriting toolkit to include Bitcoin (BTC), stablecoins, and other tokens alongside traditional assets like cash and stocks. If adopted, digital assets could be treated similarly to the “three C’s”—Credit, Capacity, Collateral—potentially introducing a “fourth C” into mortgage finance.

Background: FHFA’s Mandate and Market Context

The FHFA oversees roughly $8.5 trillion in U.S. residential mortgages through Fannie Mae, Freddie Mac, and the Federal Home Loan Banks. Traditionally, borrowers demonstrate financial strength via liquid assets held in fiat. Crypto holders have faced an extra hurdle: they must convert digital assets into USD, deposit them in a bank account, and wait months (“seasoning”) before lenders acknowledge those funds.

Regulatory Shift: SAB 121 Repeal

Until January 23, 2024, many major banks could not offer crypto‐collateralized loans due to the SEC’s SAB 121 guidance, which required publicly traded companies to record customer crypto holdings as liabilities on their balance sheets. This inflated capital requirements and discouraged such products. The SEC formally withdrew SAB 121 on that date, removing a major barrier to integrating crypto into mainstream finance.

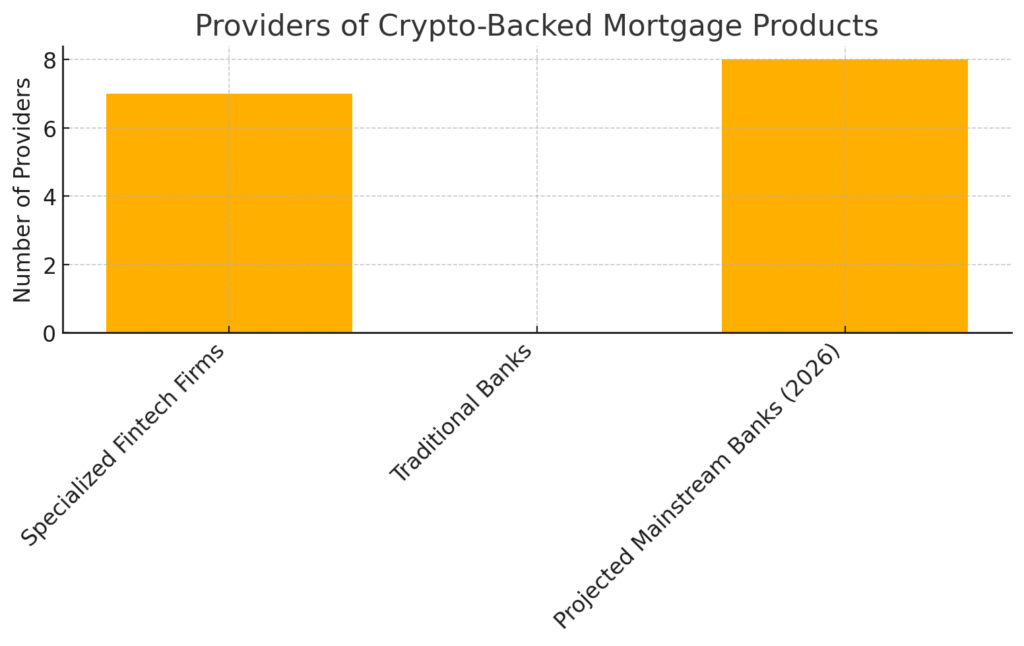

Existing Crypto‐Backed Mortgage Products

Specialized fintech firms have long offered crypto‐collateralized loans, locking up clients’ digital assets at high collateral ratios. Borrowers receive USD for home purchases or other needs, while risking margin calls if asset values decline. A chart below illustrates the current landscape of providers and projected mainstream entry:

See the bar chart “Providers of Crypto‐Backed Mortgage Products” above.

This chart shows that as of mid-2025, approximately seven specialized fintech firms offer crypto mortgage products, while traditional banks offer none. By 2026, we project up to eight mainstream banks may enter this space.

Borrower Trends: Crypto Profits in Housing Finance

A late-2024 study revealed an uptick in low-income households using crypto gains to pay down mortgages, especially in regions with high digital asset adoption. Mauricio di Bartolomeo, co-founder of BTC loan provider Ledn, noted that some Bitcoin holders purchase real estate without selling a single Satoshi, leveraging collateralized loans to maintain exposure while accessing liquidity. Many of these borrowers are high-net-worth individuals who don’t meet conventional income standards but hold substantial digital assets.

Policy Implications and Risk Considerations

Integrating crypto into mortgage underwriting raises questions around:

- Volatility Management: How to value and stress-test volatile digital assets amid market swings?

- Margin Call Policies: Defining clear protocols for collateral shortfalls to protect lenders and borrowers.

- Valuation Standards: Establishing uniform frameworks for on-chain asset valuation.

- Regulatory Oversight: Coordinating between the FHFA, SEC, and Treasury to align financial stability goals.

Industry experts suggest that standardized guidance will be essential before major banks can onboard crypto-collateral products without exacerbating credit risk.

Future Outlook: Mainstream Adoption on the Horizon

If the FHFA endorses crypto as qualifying assets, digital-native borrowers could bypass lengthy fiat–crypto conversion processes. This shift would:

- Expand Access: Open mortgage markets to millions with untapped digital wealth.

- Accelerate Product Innovation: Spur new loan structures blending DeFi principles with traditional underwriting.

- Reshape Credit Profiles: Introduce on-chain transaction history and staking yields as credit indicators.

However, widespread adoption by incumbents hinges on the FHFA’s final guidelines and risk-management frameworks.

Conclusion

The FHFA’s decision to evaluate cryptocurrency holdings for mortgage eligibility marks a watershed moment in housing finance. By potentially recognizing digital assets alongside cash and stocks, the agency is acknowledging the evolving nature of wealth in the digital economy. While challenges around volatility, valuation, and regulatory coordination remain, this development paves the way for more inclusive and efficient financing solutions. As specialized fintech pioneers continue to demonstrate workable models, the stage is set for mainstream banks to follow suit—ushering in a new era where crypto meets bricks and mortar.