Key Points :

- Bitcoin’s recent decline was driven primarily by global liquidity contraction, not weak demand

- The past 6 months reflect both overheating correction and credit tightening

- Leverage unwinding in derivatives markets accelerated downside pressure

- On-chain indicators confirm capitulation of short-term holders

- A new ATH requires liquidity expansion and institutional pathways, not just ETF momentum

- Political and structural factors—especially in the U.S. and Japan—are critical for the next cycle

1. Introduction: Beyond Price—Understanding the Structure of the Market

Bitcoin’s recent stabilization has triggered growing optimism that the market may have found a bottom. Indeed, short-covering rallies and reduced selling pressure suggest a temporary equilibrium. However, focusing solely on price misses the deeper structural story.

To understand what lies ahead, we must analyze what truly caused the past six months of decline—and more importantly, what conditions are required for Bitcoin to reach new all-time highs (ATHs).

The answer is not demand.

It is liquidity.

2. Bitcoin as the “Terminal Asset” of Global Liquidity

Bitcoin is often misunderstood as a purely demand-driven asset. In reality, it sits at the far end of a hierarchical capital flow system:

Central Bank Liquidity → Bonds → Equities → Crypto Assets

This means Bitcoin is the last recipient of global capital flows. When liquidity expands, excess capital eventually reaches crypto. When liquidity contracts, Bitcoin is among the first to suffer.

This conceptual relationship illustrates how Bitcoin price movements closely follow global liquidity cycles.

3. The Macro Shift: Why Liquidity Contracted

Over the past six months, several macroeconomic shifts converged:

- Persistently high U.S. interest rates

- Strong U.S. dollar (USD appreciation)

- Rising Japanese government bond (JGB) yields

These factors collectively triggered a global tightening of financial conditions.

The Japan Factor (Underrated but Critical)

Japan plays a unique role as one of the world’s largest external investors. Through the yen carry trade, Japanese capital has historically provided liquidity to global markets.

However, rising domestic yields weakened this mechanism:

- Japanese investors repatriated funds

- Overseas asset allocation declined

- Global liquidity supply shrank

This directly impacted Bitcoin—not because people stopped wanting it, but because capital stopped reaching it.

4. Credit Contraction and the Leverage Unwind

Liquidity contraction alone does not explain the full decline. The second layer is credit tightening, particularly in derivatives markets.

Crypto markets had accumulated significant leverage:

- High open interest in perpetual futures

- Overexposure to long positions

- Retail and institutional leverage stacking

When prices began to fall, this triggered a cascade:

- Liquidations of long positions

- Forced selling

- Feedback loops driving further decline

This is a classic deleveraging cycle, where future demand (leveraged buying) is pulled forward and then erased.

5. On-Chain Evidence: Signals of Market Stress

On-chain metrics provide strong confirmation of this structural stress.

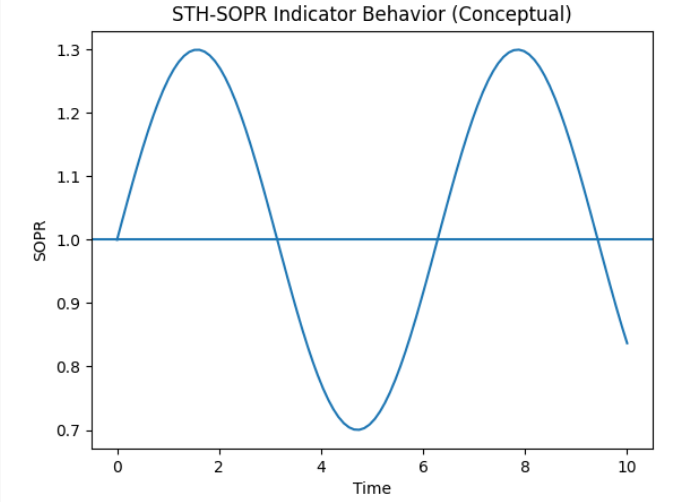

5.1 STH-SOPR (Short-Term Holder SOPR)

This metric measures whether short-term holders are selling at a profit or loss.

- Below 1 → selling at a loss (capitulation)

- Above 1 → selling at profit (healthy demand)

Over the past months, SOPR remained below 1, indicating:

- Panic selling

- Weak market confidence

- Ongoing absorption of losses

A sustained recovery above 1 would signal trend reversal.

5.2 Coinbase Premium Gap

This indicator measures price differences between U.S. exchanges and global markets.

- Positive → U.S. buying pressure

- Negative → weak institutional demand

Recent trends show persistent negative territory, suggesting:

- Lack of strong U.S. spot demand

- Institutional hesitation

6. The Misconception: ETFs Alone Cannot Drive ATH

There is a growing narrative that Bitcoin ETFs will automatically push prices higher.

This is incomplete.

ETFs are merely access channels, not sources of liquidity themselves.

Without underlying capital expansion, ETFs simply redistribute existing capital rather than introducing new inflows.

7. What Actually Drives the Next Bull Market

The path to a new ATH depends on one core condition:

Can liquidity flow back to the “edge” of the system—where Bitcoin sits?

7.1 U.S. Political and Monetary Policy

Upcoming U.S. elections will influence:

- Fiscal expansion

- Monetary easing pressure

- Regulatory clarity

If policies shift toward:

- Lower interest rates

- Increased government spending

Then global liquidity will expand again—fueling risk assets.

7.2 Japan’s Structural Role

A potential approval of a Bitcoin ETF in Japan could be transformative.

Japan holds approximately:

- ~$14 trillion equivalent in household financial assets

If even a small portion reallocates into crypto via traditional brokerage channels, this would:

- Create new capital inflow routes

- Expand the investor base

- Reduce access barriers

This is not just demand—it is infrastructure for liquidity transmission.

8. Structural Shift: From Speculation to Capital Flow Engineering

The next phase of Bitcoin’s evolution is not purely speculative.

It is about:

- Financial infrastructure

- Regulatory integration

- Institutional capital routing

Markets are transitioning from retail-driven hype cycles to macro-driven liquidity cycles.

9. Conclusion: Follow the Money, Not the Price

The past six months were not a failure of Bitcoin demand.

They were a reflection of:

- Liquidity contraction

- Credit tightening

- Structural capital withdrawal

The next rally will not be triggered by:

- Technical patterns

- Retail sentiment

- ETF headlines alone

Instead, it will depend on:

- Global liquidity expansion

- Institutional access channels

- Policy-driven capital flows

In Bitcoin markets, price is the result—not the cause.

The real signal lies in the movement of capital.